Recently, market research firm Counterpoint Research released its list of the top 10 best-selling smartphone models for Q1 2025. The iPhone 17 series claimed the top three spots, and including the iPhone 16, four Apple models made the list. In stark contrast, none of the remaining six Android models on the list were premium devices. Xiaomi was the sole Chinese brand featured—its Redmi A5 secured the tenth and final position on the Top 10 sales chart.

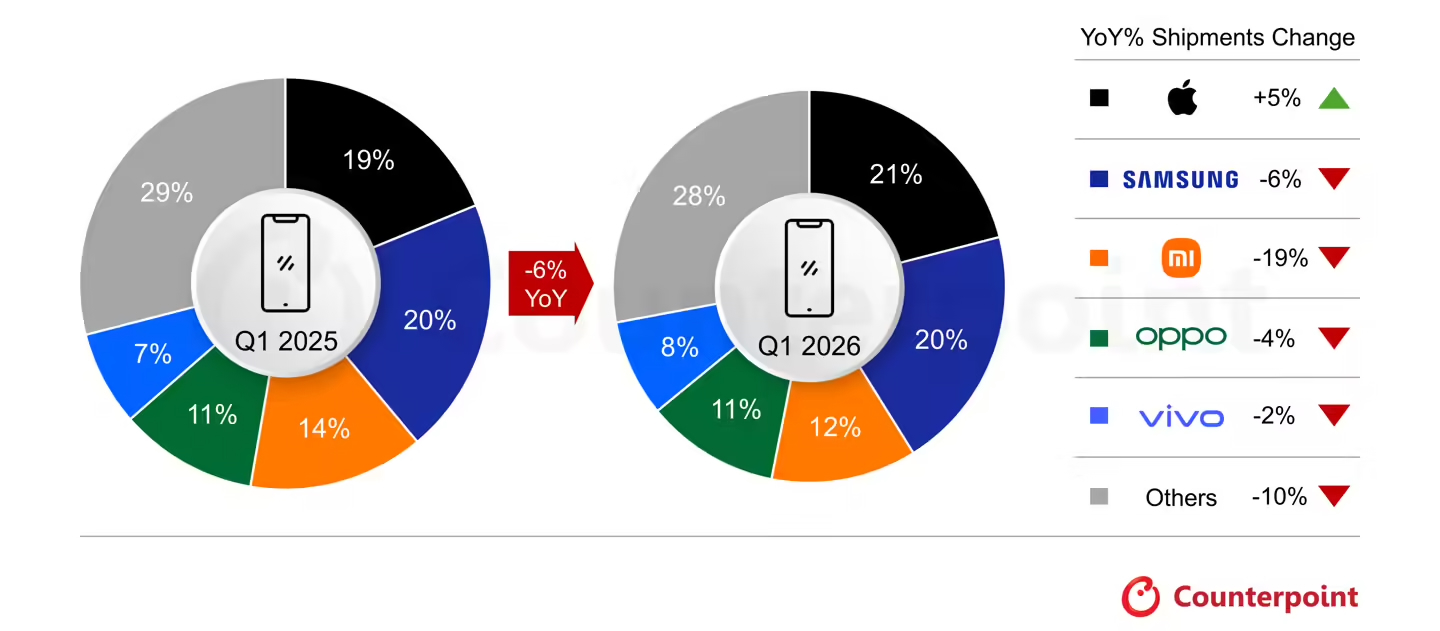

However, examining Q1’s overall global smartphone shipment data reveals a significant setback for Xiaomi. According to Counterpoint’s report, global smartphone shipments declined 6% year-on-year in Q1. Among the top five brands by market share, only Apple posted counter-cyclical growth; Xiaomi’s shipments plunged by 19%.

(Source: Counterpoint)

Xiaomi’s underwhelming smartphone performance has drawn considerable attention. Many observers believe that Xiaomi’s car-making initiative has consumed critical internal resources—including Lei Jun personally dedicating nearly all his energy to the automotive project—making it the primary cause behind the smartphone division’s sluggishness.

In LeiTech’s (ID: leitech) view, Xiaomi’s declining smartphone shipments are closely tied to broader market conditions, Xiaomi’s product portfolio strategy, and competitive positioning. Whether Xiaomi’s smartphone and automotive businesses mutually reinforce each other—or operate as a zero-sum game—is worth exploring further in our analysis below.

Shipment Decline, Yet Individual Models Performing Well

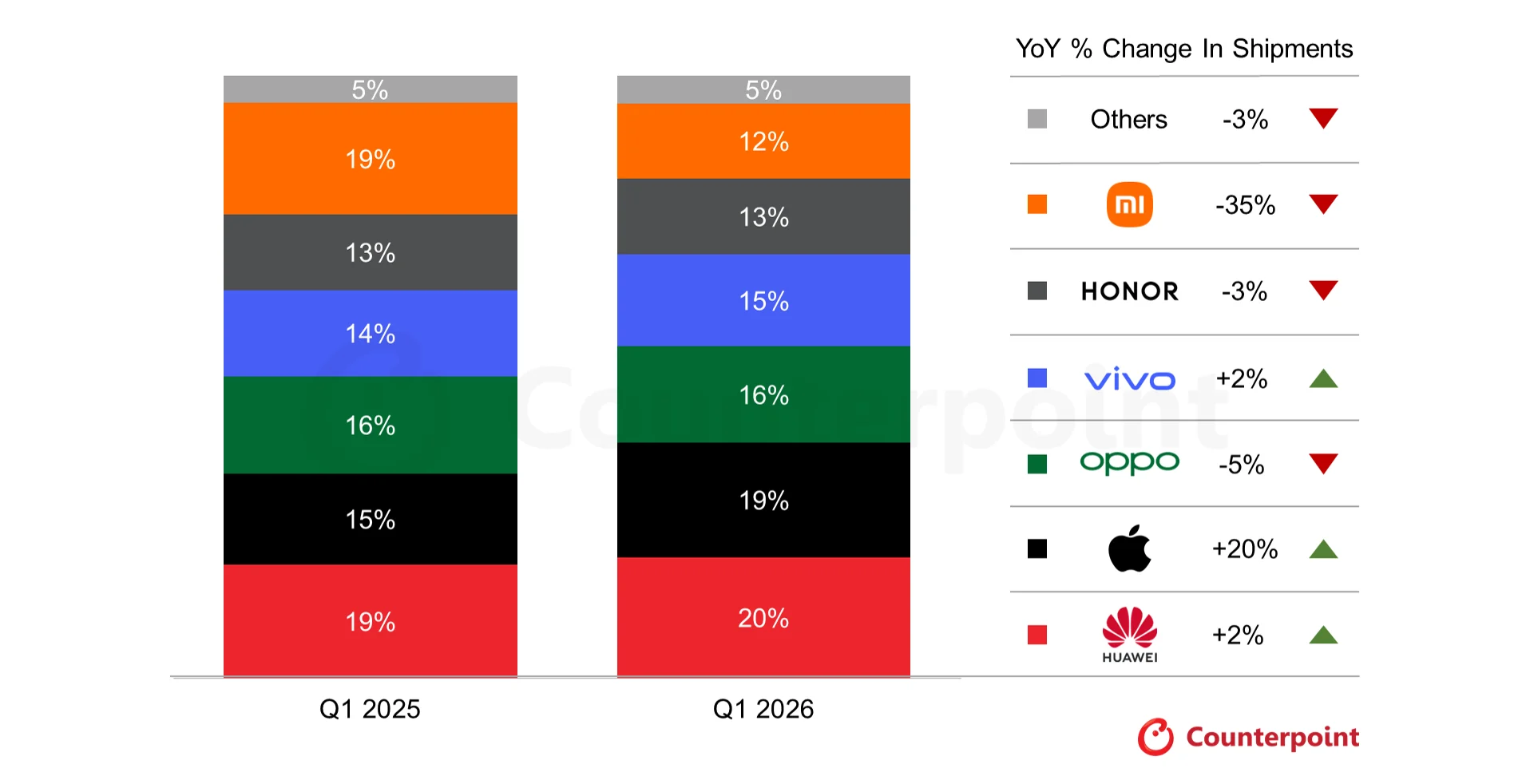

Several major market research firms recently published Q1 domestic smartphone market data. According to Counterpoint’s report, the top five brands by market share were Huawei, Apple, OPPO, vivo, and Honor. Xiaomi ranked sixth with a 12% share, falling out of the top five, and its shipments dropped 35% year-on-year.

(Source: Counterpoint)

Looking back across the entire quarter, Xiaomi executed virtually no major initiatives in its smartphone business. At January’s Mobile World Congress (MWC), Xiaomi merely re-launched its previously announced Xiaomi 17 series for overseas markets. As noted earlier, the Redmi A5—the sole Xiaomi model appearing on the Top 10 global sales list—was also launched last year. The only genuinely new device introduced during Q1 was the Redmi Turbo 5 series, unveiled in late January.

In terms of specifications and pricing, the Redmi Turbo 5 series is squarely positioned as a mid-tier offering. It features mid-range and sub-flagship chipsets, high-spec displays, and high-wattage fast charging—targeting the RMB 2,000–3,000 price bracket.

(Source: Xiaomi)

Honestly, the Redmi Turbo 5 series delivers solid product competitiveness—and its market performance has been quite strong. According to data disclosed by tech influencer @RD Observation, cumulative activations of the Redmi Turbo 5 series reached 1.191 million units by March 31.

(Source: Weibo)

Yet relying solely on the Redmi Turbo 5 series to sustain an entire brand’s quarterly shipments is clearly unrealistic. With few new models launched in Q1, Xiaomi’s sales remained heavily dependent on legacy products. Based on data from @RD Observation, the Xiaomi 17 series sold approximately 1.57 million units domestically in Q1, while the Redmi K90 series achieved roughly 1.0897 million units.

For comparison: By Q1, OPPO’s Find X9 series had accumulated ~1.64 million activations; vivo’s X300 series reached ~1.98 million; and the Xiaomi 17 series hit 4.26 million. This indicates that Xiaomi not only remains competitive in the flagship segment but also maintains a leadership position among Android vendors.

(Photograph: LeiTech)

Overall, Xiaomi’s key selling models individually exhibit no obvious flaws—and their sales figures remain respectable. However, Xiaomi lacked breakout “hit” models in Q1 capable of driving meaningful shipment growth. In fact, beyond Apple and Huawei, most other Android brands still rely heavily on budget entry-level devices to fuel volume. Xiaomi refrained from deploying a “volume-first” product strategy this quarter—making its shipment numbers appear comparatively weak.

Additionally, Xiaomi’s April activities indicate its smartphone efforts remain focused on the mid-to-high-end segment. Its latest flagship promotion centers on the Redmi K90 Max—a well-balanced sub-flagship device whose core selling point is extreme performance enabled by active fan-based cooling. Priced starting at RMB 2,999, it offers compelling value. Its launch performance was impressive: Within four hours of going on sale, it broke the one-year sales record for devices in its price range.

(Source: Xiaomi)

LeiTech (ID: leitech) believes the smartphone industry has long since matured into a saturated, low-growth market where leading brands’ offerings lack clear differentiation. Even Xiaomi—which posted relatively weak shipment figures—maintains favorable user sentiment and reputation.

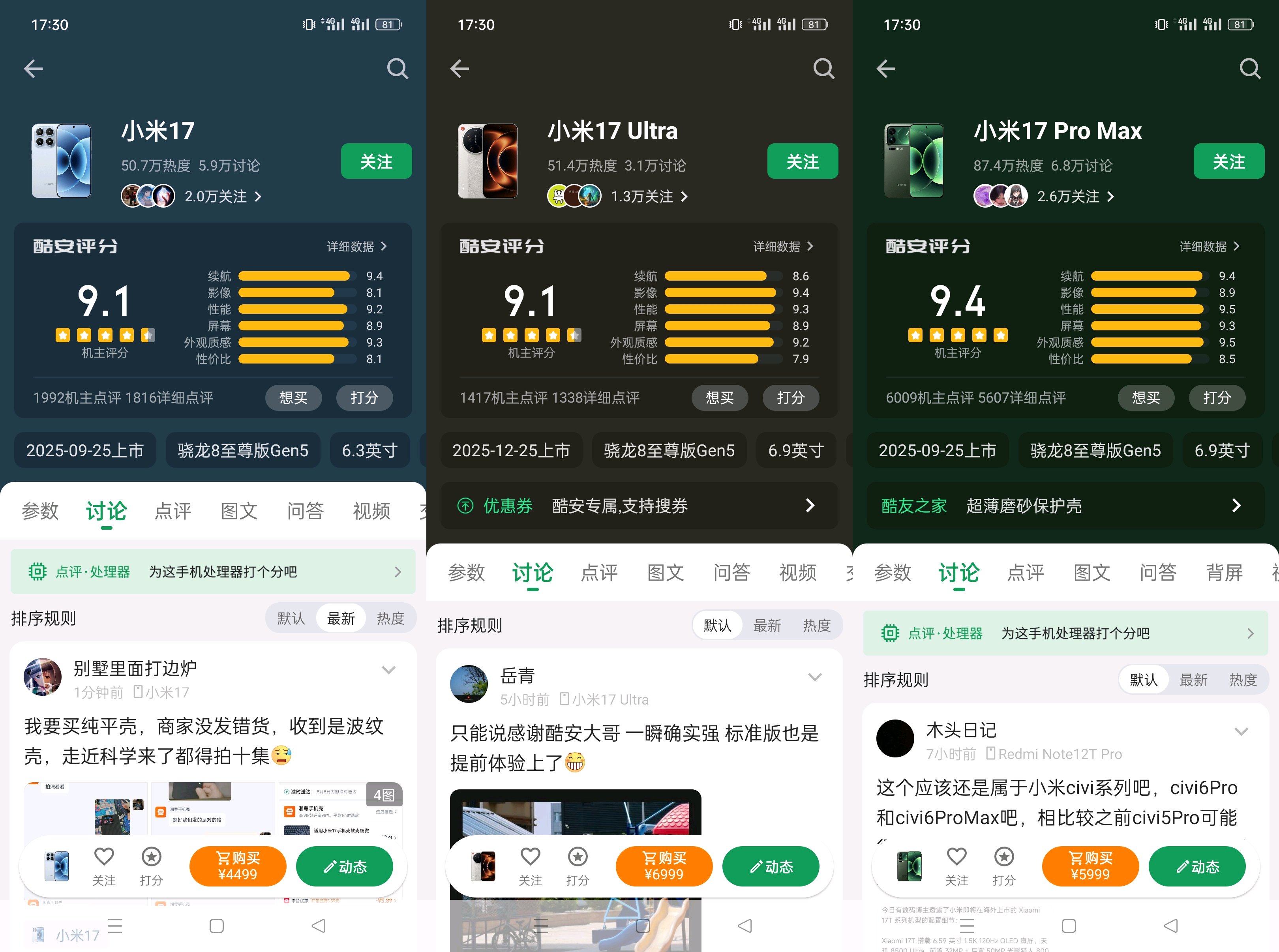

Take the Xiaomi 17 series, for example: It earned high scores on CoolAPK’s smartphone rating platform, and user feedback on e-commerce sites has been overwhelmingly positive. In our assessment, Xiaomi’s shipment decline bears little direct relationship to the inherent competitiveness of its current lineup.

(Source: CoolAPK)

Is the Automotive Business the “Prime Suspect” Behind Smartphone Weakness?

Xiaomi officially announced its automotive venture in 2021—meaning the Xiaomi Auto brand has now existed for over five years.

According to Xiaomi’s financial disclosures, its automotive business generated over RMB 100 billion in revenue and contributed more than RMB 20 billion in gross profit in 2025. By comparison, Xiaomi’s smartphone business reported RMB 186.4 billion in revenue and ~RMB 18.6 billion in gross profit for the same period. On paper, Xiaomi Auto’s profitability indeed surpasses that of its smartphone division.

Nonetheless, LeiTech (ID: leitech) contends that the automotive business has not “bled” resources from smartphones—and its impact on the mobile division is comparatively modest. Objectively speaking, smartphone and automotive supply chains operate as two largely independent systems; Xiaomi did not divert funds from phone development to fund car production due to insufficient capital.

If there is any tangible impact of automotive operations on smartphones, it lies primarily in the reallocation of marketing and PR resources. Q1 marked a critical ramp-up phase for Xiaomi Auto’s production capacity. From Lei Jun and Lu Weibing down to Xiaomi Group’s entire communications and marketing team, the overwhelming majority of resources were dedicated to the automotive business.

(Source: Weibo)

This shift is entirely understandable: For Xiaomi, automobiles remain a nascent, growth-stage business requiring intensive investment—naturally drawing focus away from the smartphone division.

In our view, the root cause behind Xiaomi’s smartphone shipment decline is unprecedented cost pressure driven by skyrocketing memory chip prices—forcing Xiaomi to adopt a cautious, conservative strategy in its smartphone business. Some may ask: If memory costs surged across the board, why was Xiaomi impacted most severely?

The answer lies primarily in Xiaomi’s distinctive product mix. Historically, Xiaomi’s smartphone shipments—especially overseas—have been dominated by entry-level models, exemplified by the Redmi A5, which appeared on the global Top 10 sales list.

Compared to premium flagships, entry-level devices are far more sensitive to cost fluctuations. Memory price hikes push already razor-thin margins on budget phones into outright losses. Thus, much of Xiaomi’s shipment decline stems from a strategic recalibration of its entry-level portfolio: Rather than selling at a loss, Xiaomi opted to discontinue unprofitable models—retaining only ultra-low-cost, margin-positive options like the Redmi A5.

(Source: Xiaomi)

By contrast, flagship models like the Xiaomi 17 series are comparatively insulated from supply-chain disruptions. Moreover, the Xiaomi 17 series enjoys tighter synergy with the automotive business—as a showcase product for Xiaomi’s “Human-Car-Home” ecosystem vision. In other words, rather than being “dragged down” by Xiaomi Auto, the Xiaomi 17 series actually benefits from the automotive brand’s premium halo effect—enhancing its competitiveness in the marketplace.

Xiaomi’s Path Forward: Weathering the Downturn and Identifying New Growth Levers

In prior analyses, we noted that Apple was least affected by the current memory chip price surge—leveraging its massive cash reserves to stockpile components and signing long-term supply agreements with memory giants like Samsung and SK Hynix.

Yet even Apple’s memory inventory appears increasingly constrained. For instance, the Mac mini (16GB + 256GB) has been discontinued, and multiple Mac models have eliminated configurations with 64GB or higher RAM. Recent leaks also suggest that while the standard iPhone 18 will avoid price hikes, it will feature lower-grade manufacturing processes—and even downgrade to inferior display panels.

In short, even Apple—the industry’s most financially robust player—must now practice stringent cost discipline amid this memory crisis. For Xiaomi and other smartphone vendors, navigating this challenge is exceptionally difficult. The core driver behind soaring memory prices is the AI arms race: AI titans are aggressively purchasing memory chips at premium prices, inevitably squeezing capacity previously allocated to consumer electronics such as smartphones, PCs, and gaming consoles.

Indeed, streamlining product portfolios, eliminating loss-making SKUs, and implementing price increases are common countermeasures adopted across the smartphone industry. Against this backdrop, consumer purchase intent is waning—and the sector faces a prolonged winter. The most prudent survival strategy involves consolidation, conservatism, and seeking new growth vectors beyond smartphones.

Currently, the automotive business stands as Xiaomi’s second-largest operational pillar—and Lei Jun’s highest-priority focus area. Crucially, Xiaomi Auto remains in a high-growth phase, poised to deliver increasing revenue and profits. In 2025, Xiaomi Auto generated over RMB 100 billion in revenue and more than RMB 20 billion in gross profit, delivering 410,000 vehicles—an explosive 200% year-on-year increase.

In Q1 2026, Xiaomi launched its next-generation SU7 series—surpassing 30,000 units sold within just three days of launch. Lei Jun has set a 2026 delivery target of 550,000 units, while institutions such as Huatai Securities forecast an even more optimistic 650,000 units. It is virtually certain that Xiaomi Auto will contribute significantly more revenue and profit in 2026—offsetting potential shortfalls in the smartphone business.

(Source: Xiaomi)

Additionally, AI represents another key domain where Xiaomi is actively investing and innovating. This year, Lei Jun and Xiaomi have markedly intensified promotional efforts around their proprietary AI technologies and products.

For example, in April, Xiaomi launched its latest large language model (LLM), MiMo-V2.5—featuring trillion-parameter scale and advanced agent capabilities—opening public beta testing and offering high-value token pricing plans. In February, Xiaomi unveiled its first-generation VLA (Vision-Language-Action) robot model, adopting a “dual-brain” architecture to balance reasoning intelligence and physical execution efficiency. Xiaomi has also invested in startup Variable Robotics.

(Source: Weibo)

On the consumer-product front, Xiaomi is advancing Agent-powered solutions like Xiaomi Claw and Super XiaoAi—integrating AI capabilities across its full “Human-Car-Home” ecosystem.

Faced with a smartphone business operating in winter conditions, Xiaomi could certainly choose to pour substantial capital into reviving its “volume-first” strategy to “rescue” sales figures—achieving modestly improved shipment metrics at the likely expense of profitability.

Between appearances (“face”) and fundamentals (“substance”), Xiaomi’s more rational, forward-looking decision is to prioritize substance: preserving and strengthening its core capabilities to endure current challenges—thus better positioning itself for sustainable long-term growth.